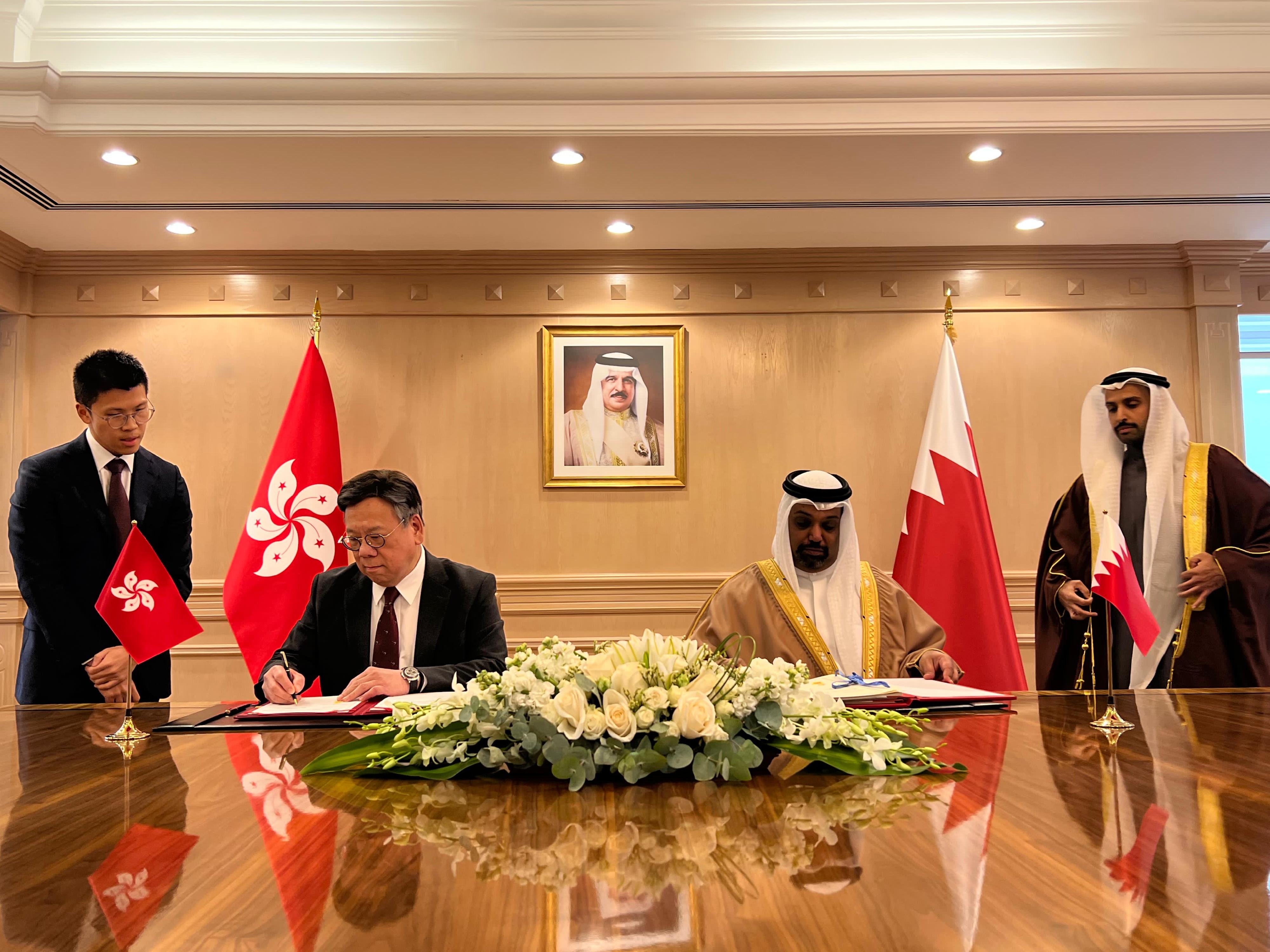

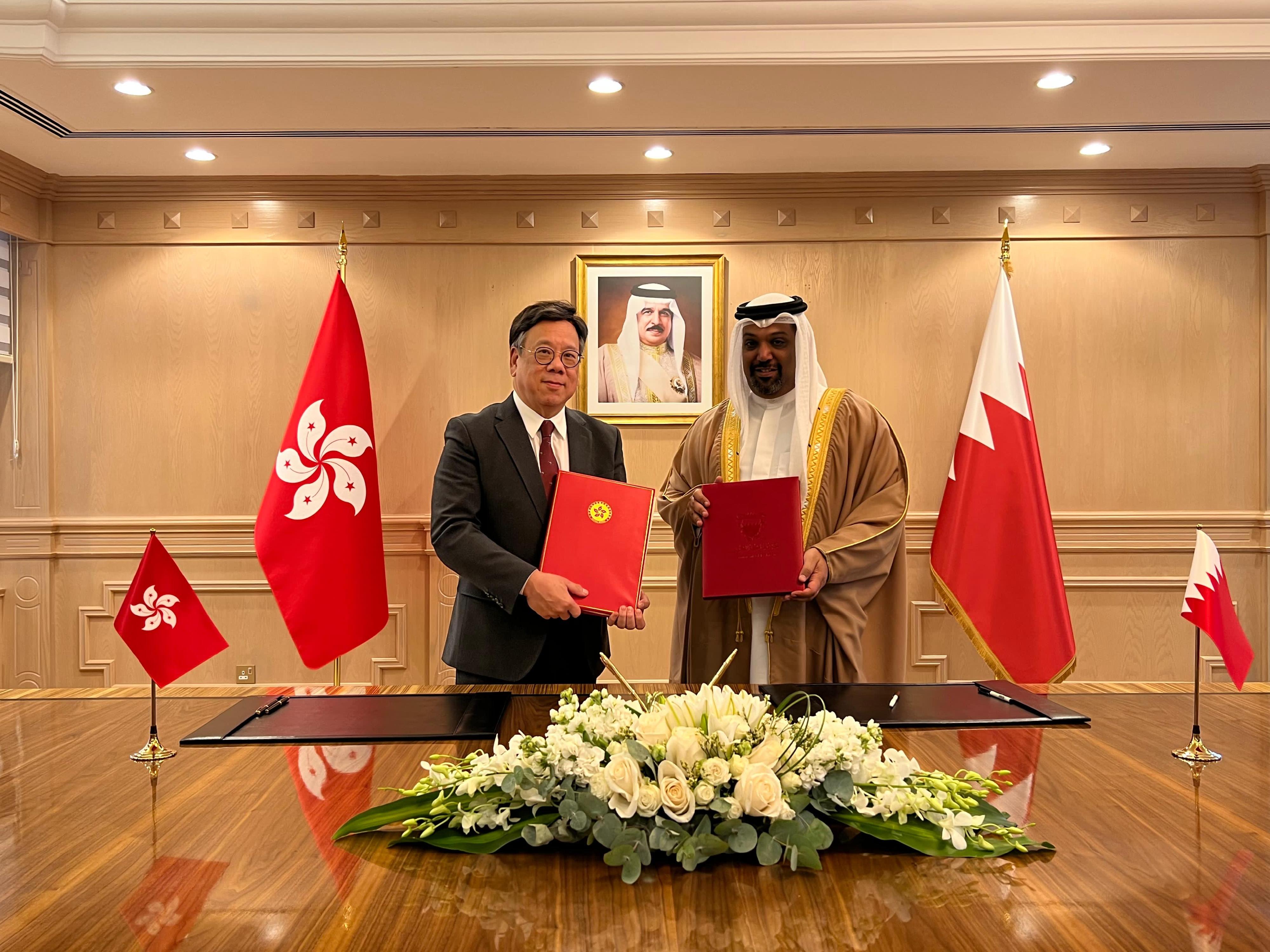

Hong Kong and Bahrain enter into tax pact (with photos)

Hong Kong yesterday (March 3, Manama time) signed a comprehensive avoidance of double taxation agreement (CDTA) with Bahrain, signifying the sustained efforts of the Hong Kong Special Administrative Region (HKSAR) Government in expanding Hong Kong's CDTA network, in particular with tax jurisdictions participating in the Belt and Road Initiative.

​ This CDTA is the 49th agreement that Hong Kong has concluded. It sets out the allocation of taxing rights between the two jurisdictions and will help investors better assess their potential tax liabilities from cross-border economic activities.

​ The Secretary for Financial Services and the Treasury, Mr Christopher Hui, said, "Bahrain is one of the economies participating in the Belt and Road Initiative. I have every confidence that this CDTA will further promote economic and trade connections between Hong Kong and Bahrain, and offer additional incentives for the business sectors of both sides to do business or make investments. Hong Kong will continue to negotiate with trading and investment partners with a view to expanding its CDTA network. This could enhance the attractiveness of Hong Kong as a business and investment hub, and consolidate the city's status as an international economic and trade centre."

​ Under the Hong Kong-Bahrain CDTA, Hong Kong companies can enjoy double taxation relief in that any tax paid in Bahrain, whether directly or by deduction, in accordance with the CDTA will be allowed as a credit against the tax payable in Hong Kong in respect of the same income, subject to the provisions of the tax laws of Hong Kong.

​ The Secretary for Commerce and Economic Development, Mr Algernon Yau, who was on an official visit to Manama, signed the CDTA with Bahrain on behalf of the HKSAR Government. Representing the Government of Bahrain was the Minister of Finance and National Economy of Bahrain, Shaikh Salman bin Khalifa Al Khalifa.

​ This CDTA will come into force after the completion of ratification procedures by both jurisdictions. In the case of Hong Kong, it will be implemented by way of an order to be made by the Chief Executive in Council under the Inland Revenue Ordinance (Cap. 112). The order is subject to negative vetting by the Legislative Council.

​ Details of the Hong Kong-Bahrain CDTA can be found on the Inland Revenue Department website (www.ird.gov.hk/eng/pdf/Agreement_Bahrain_HongKong.pdf).