Questions and Answers on a Fair and Efficient Tax System in the EU for the Digital Single Market

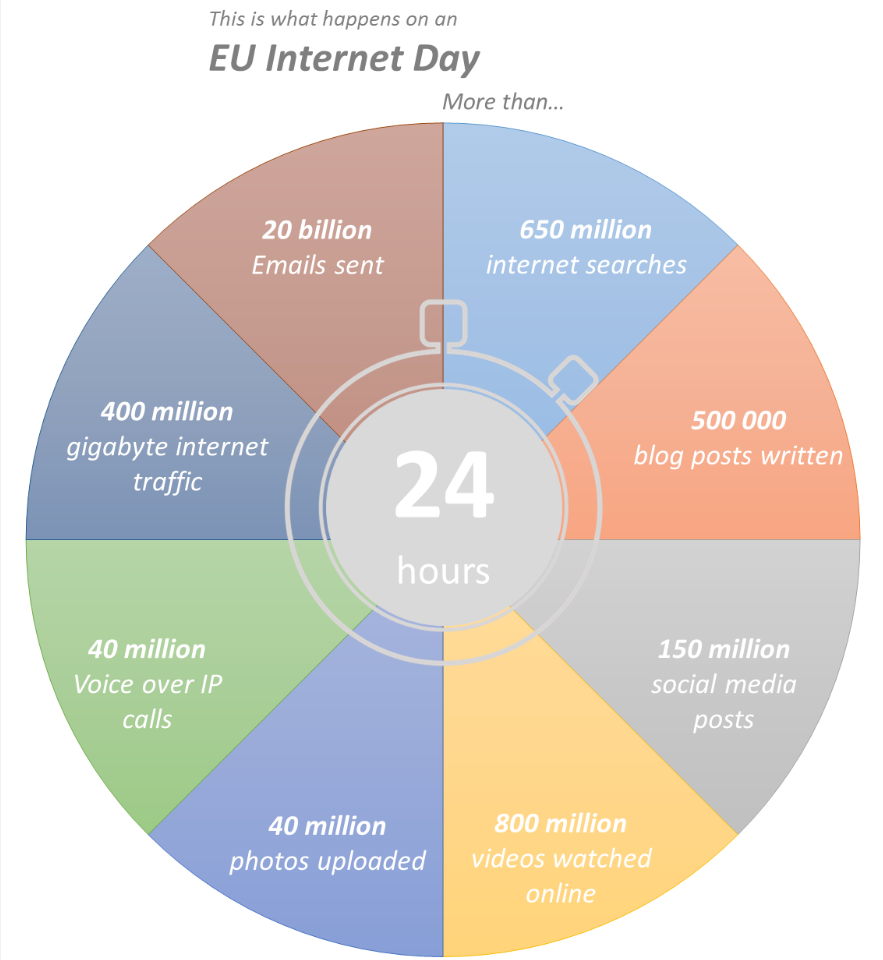

Every day, 20 billion emails and 150 million social media posts are written, and 650 million online searches are carried out in the EU. These statistics show how much the internet has transformed our lives. Yet not everything has kept pace: global corporate tax rules are over one hundred years old and are out of step with the boom in the digital economy. They were designed for ‘brick-and-mortar’ businesses, meaning that a company should be physically present in a country to be taxed there. Companies that do business and generate value online are now growing far quicker than the economy at large, yet today’s rules cannot effectively tax profits generated largely from consumer data.

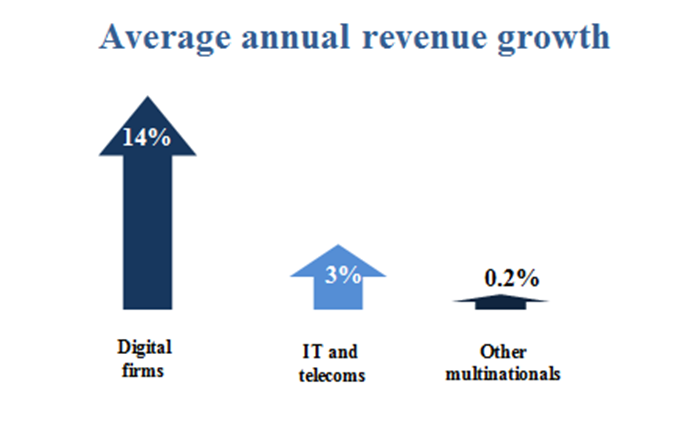

The EU has embraced the development of the digital economy, which is making a great contribution to economic growth. But this has also created a major fiscal distortion: the effective tax rate for digital companies – such as social media companies, collaborative platforms and online content providers – is around half that of traditional companies – and often much less.On average, digitalised businesses face an effective tax rate of only 9.5%, compared to 23.2% for traditional business models.

At the same time, EU Member States are under increased political pressure to ensure that all businesses – both digital and traditional – pay their fair share of tax. There is a real risk to Member State tax revenues if profits made by digital companies cannot be taxed. Last September, EU finance ministers called for a common EU solution to tackle the challenges of digital taxation, a call echoed by EU leaders in October 2017. The European Parliament has also demanded quick and ambitious action on digital taxation.

EU citizens and business are also calling for Member States and the Commission to take action to improve the fairness of tax systems. Nearly three-quarters (74%) of citizens want EU action to fight against tax avoidance. In a recent public consultation, three quarters of respondents agreed that current international taxation rules allow companies with digital business models to benefit from certain favourable tax regimes and push down their tax contributions. Some 82% believed that something should be done.

The taxation of the digital economy is a key part of the Commission’s fair taxation agenda with President Juncker noting the need for digital companies to pay their fair share of taxes in his 2017 State of the Union speech. In its Communication last September, the Commission committed to examining the options for digital taxation with a view to developing a common EU approach.

(Source: Commission services based on InternetLiveStats.com)

Today’s package complements the extensive work already done at EU level in recent years to ensure fair, effective and growth-friendly corporate taxation in the Single Market. It supports the Commission’s key priority of completing the Digital Single Market. The EU proposals for taxing the digital economy should also provide inspiration and create momentum for the ongoing international work on digital taxation, steered by the G20 and OECD. At the same time, the solution at EU level must also take into account the global dimension: the OECD has committed to bring forward a report on the next steps internationally by 2020. By being a first adopter of digital tax solutions, the EU can be at the forefront in shaping the global response.

What are the main problems?

Today’s international corporate tax rules are not fit for the realities of the modern global economy and do not capture business models that can make profit from digital services in a country without being physically present. Current tax rules also fail to recognise the new ways in which profits are created in the digital world, in particular the role that users play in generating value for digital companies. As a result, there is a disconnect – or ‘mismatch’ – between where value is created and where taxes are paid.

Given the rapid pace at which the digital economy is growing, this situation poses several risks that should be tackled urgently:

– The system is unfair and there’s no level playing field as traditional companies tend to carry a heavier tax burden than digital ones. Today’s tax systems give an advantage to digital business models for a variety of reasons. In some cases this is intentional, for example to foster digitalisation and R&D activities. But in other cases, mismatches and loopholes between different national systems, combined with the mobile and ‘virtual’ nature of digital businesses, reduce the tax burden much more than expected. It is quite common for digital companies to have tax levels close to zero in countries where they have a significant market share.

– Member States’ tax revenues are at risk if they cannot tax profits from digital activities. EU countries are under increasing pressure to take action to tax the digital economy, in order to safeguard public finances that pay for schools, hospitals and transport and ensure a level playing field. Several EU countries are already taking unilateral action, creating inconsistencies and loopholes in the Single Market and making it a legal minefield for companies.

– Digital companies need a stable, competitive environment to thrive. The EU needs modern, fair and growth-friendly tax rules to support the growth of the Digital Single Market. Above all else, companies need a stable, predictable environment and one set of rules across the EU to do business.

What are you proposing?

Today’s package consists of:

– A common EU solution for the taxation of the digital economy in the EU, enabling Member States to tax profits made in their territory, even if a company does not have a physical presence there. The new rules would ensure that online businesses contribute to public finances at the same level as traditional ‘brick-and-mortar’ companies. This proposal is accompanied by a Recommendation to Member States to amend their Double Taxation Treaties with third countries so that the same rules apply to EU and non-EU companies. The Commission has offered to assist Member States with exploratory talks on implementing the digital corporate tax update at international level.

– A new interim tax for digital services, which would apply to the most urgent gaps and loopholes in the taxation of digital activities. The measure ensures that those activities which are not currently effectively taxed would begin to generate immediate revenues for Member States.

Why is the taxation of the digital economy such an urgent global issue?

Digital companies are growing far faster than the economy at large, and this trend is set to continue. In 2006, only one digital company was in the top 20 firms by market capitalisation, whereas by 2017 this had risen to 9 digital companies. The challenge is to make the most of these digital opportunities to ensure Europe’s competitiveness, while ensuring fair taxation. Profits should be taxed where the value is created. However, how the value is created has evolved with new business models while the rules for taxing profits have remained the same. This makes it very difficult to tax profits where the value is created from digital activities.

Value Creation in the Digital Economy

In the digital economy, value is often created from a combination of algorithms, user data, sales functions and knowledge. For example, a user contributes to value creation by sharing his/her preferences (e.g. liking a page) on a social media forum. This data will later be used and monetised for targeted advertising. The profits are not necessarily taxed in the country of the user (and viewer of the advert), but rather in the country where the advertising algorithms has been developed, for example. This means that the user contribution to the profits is not taken into account when the company is taxed.

How does this fit in with international work?

The EU wants to create momentum behind the ongoing international work on digital taxation. In its Communication last September, the Commission stressed that the ideal solution to taxing the digital economy would be at global level. Member States agreed with this in their discussions and conclusions on digital taxation last year. The EU has been actively supporting the OECD’s work on this issue, and is keen to see ambitious and effective solutions implemented internationally. The OECD’s report to the G20 in April will be an important step in that direction.

But progress at international level on digital taxation is challenging. The EU cannot afford to delay any longer, given the growing number of problems related to digital taxation. In line with calls of EU leaders, the Commission has proposed EU solutions for the fair and effective taxation of the digital economy.

In developing these proposals, the Commission was in close and regular contact with the OECD, G20 and other international partners, to keep the EU and global approach as aligned as possible. The EU proposal should feed the international debate and help push our global partners into action by providing a clear example of how the principles under discussion at international level can be transformed into a modern, fair and efficient corporate taxation framework adapted to the digital era.

The Commission has taken into account the parameters agreed at global level, as well as existing Member State practices in designing the interim solution.

Will consumers have to bear the cost of new tax measures for the digital economy?

There is no reason why this should happen, provided that companies behave responsibly towards their customers. The Commission’s goal is to ensure that all companies contribute their fair share to public revenue. This aim is to secure a level playing field between different types of companies, which is important for fair competition. Pushing out competitors by offering low prices that are compensated through tax dumping is not a sustainable situation for companies.

Are these proposals compatible with the EU’s Digital Single Market?

Yes. By proposing a fair and effective EU solution to digital taxation, the Commission aims to improve certainty, stability and ease of business for companies in the Digital Single Market. A common EU approach will prevent a patchwork of uncoordinated national measures from creating new barriers for companies and distorting competition in the Digital Single Market.It will ensure a level playing field in the Single Market so that all companies – large or small, more or less digitalised – pay their fair share of tax. However, today’s proposals will also ensure that digital start-up and scale-up companies are not unduly burdened. The proposed thresholds will ensure that only the largest businesses that have a significant digital presence or make large amounts of revenue in EU Member States will come under the scope of the new rules.

Fair and effective taxation is essential to support the Digital Single Market. It cannot reach its full potential if young and innovative companies are held back by antiquated tax rules. The Digital Single Market could contribute €415 billion to the European economy, boosting jobs, growth, competition, investment and innovation. The value of the data economy in the EU will increase to €739 billion by 2020, representing 4% of overall EU GDP. With digitalisation, cross-border opportunities for even the smallest companies will increase.

Do the new proposals discriminate against non-EU digital companies?

The new rules do not target or ring-fence any individual companies, sector or nationality. The common structural approach covers all companies, both EU and non-EU that have a significant digital presence in the Union. Any EU company or non-EU company located in a country where there is no applicable double tax treaty, with a significant digital presence in a Member State will be subject to taxation on its digital activities. Similarly, the interim tax is designed in a way that it includes both EU and non-EU companies. Our goal is to ensure a level-playing field for all businesses operating in the EU, large or small, more or less digitalised.

A COMMON EU SOLUTION FOR TAXING THE DIGITAL ECONOMY

What are the key elements of the common EU solution to taxing the digital economy, proposed by the Commission?

Under the proposed new rules, Member States will be able to tax profits that are generated in their territory, even if these companies do not have a physical presence there. A company will be considered to have a significant digital presence in a Member State if it fills one of the following criteria:

– It exceeds a threshold of €7 million in annual revenues from digital services in a Member State

– It has more than 100,000 users who access its digital services in a Member State in a taxable year

– Over 3000 business contracts for digital services are created between the company and business users in a taxable year.

This reform addresses two of the main problems that Member States encounter when it comes to taxing digital activities:

- First, it will no longer be necessary for a company to be physically present in a Member State in order for it to be taxed. A significant digital presence will allow Member States to tax profits generated in their territory.

- Second, factors such as user data will now be taken into account in the allocation of profits, since they play an increasingly important role in companies’ value creation. Today’s proposal changes the system for allocating taxable profits, to better reflect the different ways in which digital companies create value.

What does the Commission propose on allocating digital profits and how is this different from today’s rules and the CCCTB?

The proposed rules lay down the general principles for allocating profits to a significant digital presence. These build on the current corporate tax rules which look at the risks managed, the functions performed and the assets used by a permanent establishment and the criteria for allocating profits. Today’s proposal also includes additional tests in the profit allocation process to reflect the fact that a significant part of a digital business’ value is created where users are based and data is collected. This means that the market value of user data or of digital services could be taken into account when allocating profits to tax in the future.

While this broad reform of the current corporate tax rules is a standalone Directive, which would operate independent of other tax frameworks, the measure could eventually be integrated into the scope of the Common Consolidated Corporate Tax Base (CCCTB). The proposed CCCTB is considered the optimal solution to create fairer and more efficient taxation in the EU. It provides a solid EU framework for revised permanent establishment rules. Adapting the CCCTB in line with today’s proposed new rules would ensure that it effectively captures the digital activities of multinational companies too. The Commission stands ready to work with Member States and the European Parliament to make this happen. The Parliament’s reports on the CCCTB are a good basis for further work.

Why has the Commission recommended that Member States adapt their Double Tax Treaties with non-EU countries in line with today’s proposal?

This broad reform of the EU’s corporate tax system would supersede double taxation treaties between Member States. The proposed new rules will also apply if a Member State does not have a double taxation treaty with a third country.

However, when Member States have double tax treaties with third countries, the proposed new rules will not apply. This means that, unless the tax treaties are adapted, the new provisions will not apply in situations where a business with EU users is tax resident outside the EU. This could disrupt the level playing field between EU and non-EU businesses. Tax treaties are an area of national sovereignty, which is why the Commission has issued a Recommendation to Member States to take the necessary measures. The Recommendation states that Member States should make the following changes to their Double Tax Treaties:

- change the definition of a ‘permanent establishment’ to take into account situations where a company has a significant digital presence in given country/jurisdiction.

- include rules for how profits should be attributed to a significant digital presence, in line with the provisions proposed by the Commission.

The Commission also stands ready to help Member States identify the key third countries to prioritise in their negotiations to implement this solution at international level. This may help to ensure a smooth and consistent approach by all Member States.

Double Tax Treaties

Different countries have their own tax laws. If you are resident in one country and have income and gains from another, you may have to pay tax on the same income in both countries. This is known as ‘double taxation’. To avoid companies from being taxed twice on the same income, the allocation of taxing rights between two countries is laid down in bilateral double tax treaties. These treaties lay down the rules of ‘where to tax’, i.e. what triggers a right to tax in a country, and ‘how much to tax’, i.e. how much of corporate income is allocated to a country.

Why has the Commission proposed an interim tax?

THE INTERIM SOLUTION

The interim tax would target the most urgent gaps and loopholes in the taxation of digital activities. The measure ensures that those activities which are not currently effectively taxed would begin to generate immediate revenues for Member States. The aim is to ensure a level playing for all businesses, whether EU or non-EU based, large or small, more or less digitalised.

Today’s proposal for an interim digital tax will discourage Member States from seeking their own divergent solutions to the challenges they face which would create a patchwork of national solutions, risking the fragmentation of the Single Market. A significant number of Member States have already started to take such measures.

If agreed first, this measure would only apply until Member States have agreed and implemented the more forward-looking proposed reforms to their corporate tax systems.

How will the tax work?

The interim tax will apply to two main types of digital services, which would not be able to exist in their current form without user involvement. The common feature of such services is that they are heavily reliant on the exploitation of user participation or data obtained from users as a way to generate revenues.

- Firstly, it will cover services where the main value is created by user data, either through advertising or by the sale of the data collected by companies such as social media or search engines.

- Secondly, it will cover services of supplying digital platforms that facilitate interaction between users, who can then exchange goods and services via the platform (such as peer-to-peer sales apps).

The proposal for an interim tax focuses on activities with the biggest gap between the value created and Member States’ ability to tax them – essentially where user participation and user contribution plays a central role in value creation. The tax will be collected by the Member States where the users are located. A number of countries already have a similar tax in place, including Israel, India and some US states.

This interim measure ensures that those activities which are currently not effectively taxed would begin to generate immediate revenues for Member States. Revenues would be collected by the Member States where the users are located, and will only apply to companies with total annual worldwide revenues of €750 million and annual EU revenues of €50 million. The first threshold will limit the tax to companies of a certain scale and ensure legal certainty for companies and tax authorities in determining who is liable for tax. At the same time, it will help to ensure that smaller start-ups and scale-up businesses remain unburdened. The second threshold will ensure that the tax only applies to companies with a significant digital footprint in the EU.

An estimated €5 billion in revenues a year could be generated for Member States if the tax is applied at a rate of 3%. This single rate, once applied throughout the EU would help to avoid “tax shopping” and distortions in the Single Market. The proposed rate of 3% was chosen after a careful analysis of many different factors and impacts, including the tax burdens of businesses with different margins.

This tax will apply only as an interim measure, until the updated corporate tax rules to underpin the digital economy have been implemented.

How exactly will Member States know when the tax is due and how will they collect it?

As with all other taxes, the interim tax is based on a system of self-declaration by taxpayers. Member States will be able to carry out tax audits to check that taxpayers are fulfilling their obligations (as they do in the traditional economy). A digital portal, known as the One-Stop-Shop, system will be set up to help companies comply. As part of that system, one Member State will be responsible for identifying the taxpayer, collecting the tax and allocating it to other Member States as appropriate.

Is there a risk of double taxation and new administrative burdens with the interim tax?

The retained approach does not breach any double tax treaties with third countries or WTO rules. It remains fully grounded on the most basic principle of corporate taxation – namely, that profits should be taxed where value is created. Moreover, the Commission has included measures in the proposal to mitigate the risk of double taxation. Companies will be able to deduct the tax as a cost from their corporate tax base, alleviating the risk of being taxed twice on the same income. At the same time, simply by introducing this coordinated EU tax, the Commission is averting the risk of new burdens for business due to interim unilateral measures in individual countries.

Furthermore, the tax proposed today has a relatively simple structure and additional compliance costs will be quite limited. The tax will also only apply to businesses that exceed the thresholds of revenues for specific activities, so SMEs will not be affected. The online One Stop Shop system should also help businesses that have to pay the tax in more than one Member State.

When will the interim tax be wound down? How will the transition be handled?

The tax is intended as a temporary solution to help Member States claw back some revenues and to address the immediate risks to EU competitiveness, while the common EU solution is being discussed, developed and implemented by Member States.

The more holistic solution will give Member States the right to tax digital activities vianew corporate taxation rules and will also capture the concept of ‘user value creation’ – to which the interim tax applies. Therefore, there will be no need for it to remain in place once the final, permanent tax rules for the digital economy have been implemented.

Fair Taxation: Commission puts in place first EU counter-measures on listed non-cooperative tax jurisdictions

Guidelines adopted today mark the first step in stopping the transit of EU funds through non-cooperative tax jurisdictions. They will ensure that EU funds do not inadvertently contribute to global tax avoidance.

Today’s guidelines should guarantee in particular that EU external development and investment funds cannot be channelled or transited through entities in countries on the EU’s common list. The first-ever list was agreed and published in December 2017 and is being updated on a continuous basis.

The new requirements seek to align the EU’s objective of tackling tax avoidance at the global level with the rules governing the use of EU funds by International Financial Institutions (IFIs) such as the European Investment Bank (EIB), development financial institutions (DFIs) – including the European Fund for Sustainable Development (EFSD) – and other eligible counterparties.

Pierre Moscovici, Commissioner for Economic and Financial Affairs, Taxation and Customs Union said: “The EU’s blacklist of tax havens is a living document and more countries will be added if they don’t live up to the commitments they have made to improve their tax systems. The Commission will not allow EU funds to contribute to global tax avoidance. These EU level countermeasures should act as a wake-up call for those jurisdictions as they show the EU is serious about tackling tax avoidance on a global scale.“

Today’s guidelines set out the applicable legislation on how EU funds should be treated when it comes to tax avoidance and non-cooperative jurisdictions. They provide information on how its partners should assess projects that involve entities in jurisdictions listed by the EU as non-cooperative for tax purposes. This assessment includes a series of checks that should pinpoint a risk of tax avoidance with a business entity. For example, before channelling funding through an entity, it should be established that there are sound business reasons for how a project is structured that do not take advantage of the technicalities of a tax system or of mismatches between two or more tax systems for the purpose of reducing a tax bill.

The new guidelines will ensure that the rules are interpreted and applied consistently. In order to safeguard the EU’s development policy, an exception is made for direct financing, where a project is physically implemented in a listed non-cooperative tax jurisdiction and is not linked to money-laundering, terrorism financing, tax fraud or tax evasion.

The Commission also calls on international financial institutions and other bodies involved in the management of the EU budget to review their internal policies on non-cooperative jurisdictions in the course of 2018. This is to ensure that these policies reflect the EU’s long-standing efforts to tackle tax avoidance, both within the Union and beyond.

Background

Following the Commission’s Communication on an External strategy for Effective Taxation in January 2016, four legal acts concerning the use of EU funds by implementing partners currently contain, or will contain in the near future, the requirement that EU funds do not support projects contributing to tax avoidance. Implementing partners, such as International Financial Institutions (IFIs), development financial institutions (DFIs), or other types of eligible counterparties involved in the indirect management of the EU budget, are required to comply with these requirements when using EU funds in their investment operations. These provide a robust framework to ensure that EU funding is routed according to good governance standards in the field of taxation; particularly when coupled with existing prohibitions on the use of non-cooperative jurisdictions and the publication of the EU common list of non-cooperative jurisdictions for tax purposes.

This Communication aims to assist these organisations in ensuring compliance with the new legal provisions while also providing broader recommendations on how to assess tax avoidance issues.

In addition to the EU provisions, the Commission has encouraged Member States to agree on coordinated sanctions to apply at national level against the listed jurisdictions. Member States have already agreed on a set of countermeasures which they can choose to apply against the listed countries, including increased monitoring and audits, withholding taxes, special documentation requirements and anti-abuse provisions. The Commission will support Member States’ work to develop a more binding and definitive approach to sanctions for the EU list in 2018.

For More Information

DG ECFIN Web Page and legal texts

EU common list of non-cooperative jurisdictions for tax purposes

Communication on an External strategy for Effective Taxation

Digital Taxation: Commission proposes new measures to ensure that all companies pay fair tax in the EU

The European Commission has today proposed new rules to ensure that digital business activities are taxed in a fair and growth-friendly way in the EU. The measures would make the EU a global leader in designing tax laws fit for the modern economy and the digital age.

The recent boom in digital businesses, such as social media companies, collaborative platforms and online content providers, has made a great contribution to economic growth in the EU. But current tax rules were not designed to cater for those companies that are global, virtual or have little or no physical presence. The change has been dramatic: 9 of the world’s top 20 companies by market capitalisation are now digital, compared to 1 in 20 ten years ago. The challenge is to make the most of this trend, while ensuring that digital companies also contribute their fair share of tax. If not, there is a real risk to Member State public revenues: digital companies currently have an average effective tax rate half that of the traditional economy in the EU.

Today’s proposals come as Member States seek permanent and lasting solutions to ensure a fair share of tax revenues from online activities, as urgently called for by EU leaders in October 2017. Profits made through lucrative activities, such as selling user-generated data and content, are not captured by today’s tax rules. Member States are now starting to seek fast, unilateral solutions to tax digital activities, which creates a legal minefield and tax uncertainty for business. A coordinated approach is the only way to ensure that the digital economy is taxed in a fair, growth-friendly and sustainable way.

Two distinct legislative proposals proposed by the Commission today will lead to a fairer taxation of digital activities in the EU:

- The first initiative aims to reform corporate tax rules so that profits are registered and taxed where businesses have significant interaction with users through digital channels. This forms the Commission’s preferred long-term solution.

- The second proposal responds to calls from several Member States for an interim tax which covers the main digital activities that currently escape tax altogether in the EU.

This package sets out a coherent EU approach to a digital taxation system which supports the Digital Single Market and which will feed into international discussions aiming to fix the issue at the global level.

Valdis Dombrovskis, Vice-President for the Euro and Social Dialogue said: “Digitalisation brings countless benefits and opportunities. But it also requires adjustments to our traditional rules and systems. We would prefer rules agreed at the global level, including at the OECD. But the amount of profits currently going untaxed is unacceptable. We need to urgently bring our tax rules into the 21st century by putting in place a new comprehensive and future-proof solution.”

Pierre Moscovici, Commissioner for Economic and Financial Affairs, Taxation and Customs added: “The digital economy is a major opportunity for Europe and Europe is a huge source of revenues for digital firms. But this win-win situation raises legal and fiscal concerns. Our pre-Internet rules do not allow our Member States to tax digital companies operating in Europe when they have little or no physical presence here. This represents an ever-bigger black hole for Member States, because the tax base is being eroded. That’s why we’re bringing forward a new legal standard as well an interim tax for digital activities.”

Proposal 1: A common reform of the EU’s corporate tax rules for digital activities

This proposal would enable Member States to tax profits that are generated in their territory, even if a company does not have a physical presence there. The new rules would ensure that online businesses contribute to public finances at the same level as traditional ‘brick-and-mortar’ companies.

A digital platform will be deemed to have a taxable ‘digital presence’ or a virtual permanent establishment in a Member State if it fulfils one of the following criteria:

– It exceeds a threshold of €7 million in annual revenues in a Member State

– It has more than 100,000 users in a Member State in a taxable year

– Over 3000 business contracts for digital services are created between the company and business users in a taxable year.

The new rules will also change how profits are allocated to Member States in a way which better reflects how companies can create value online: for example, depending on where the user is based at the time of consumption.

Ultimately, the new system secures a real link between where digital profits are made and where they are taxed. The measure could eventually be integrated into the scope of the Common Consolidated Corporate Tax Base (CCCTB) – the Commission’s already proposed initiative for allocating profits of large multinational groups in a way which better reflects where the value is created.

Proposal 2: An interim tax on certain revenue from digital activities

This interim tax ensures that those activities which are currently not effectively taxed would begin to generate immediate revenues for Member States. It would also help to avoid unilateral measures to tax digital activities in certain Member States which could lead to a patchwork of national responses which would be damaging for our Single Market.

Unlike the common EU reform of the underlying tax rules, this indirect tax would apply to revenues created from certain digital activities which escape the current tax framework entirely. This system will apply only as an interim measure, until the comprehensive reform has been implemented and has inbuilt mechanisms to alleviate the possibility of double taxation.

The tax will apply to revenues created from activities where users play a major role in value creation and which are the hardest to capture with current tax rules, such as those revenues:

– created from selling online advertising space

– created from digital intermediary activities which allow users to interact with other users and which can facilitate the sale of goods and services between them

– created from the sale of data generated from user-provided information.

Tax revenues would be collected by the Member States where the users are located, and will only apply to companies with total annual worldwide revenues of €750 million and EU revenues of €50 million. This will help to ensure that smaller start-ups and scale-up businesses remain unburdened. An estimated €5 billion in revenues a year could be generated for Member States if the tax is applied at a rate of 3%.

Next Steps

The legislative proposals will be submitted to the Council for adoption and to the European Parliament for consultation. The EU will also continue to actively contribute to the global discussions on digital taxation within the G20/OECD, and push for ambitious international solutions.

For more information

DG TAXUD webpage on digital taxation